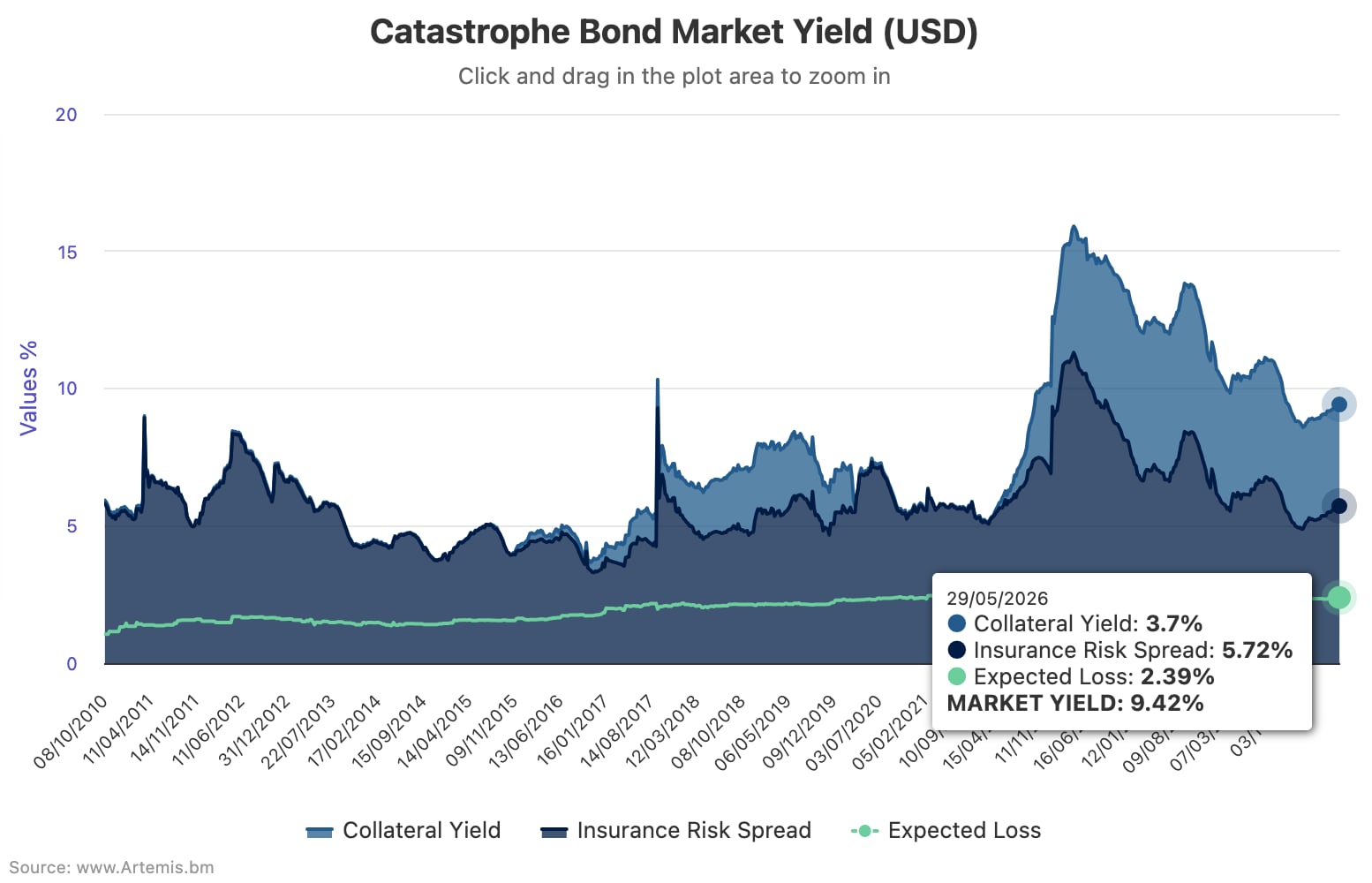

The overall catastrophe bond market yield or coupon available to investors continued to rise through May, as expected seasonal spread widening lifted total returns to 9.42% by May 29th. But this remains ~14% behind the level seen a year earlier due to softer pricing across reinsurance and cat bonds, the latest data from Plenum Investments shows.

Cat bond risk spreads began moving slowly higher in February and this trend has now continued through to late May with slow-paced seasonal widening of spreads.

It has driven the overall cat bond market yield coupon steadily higher through 2026, having stood at around 8.80% at the end of December 2025, then rising to 8.87% by the end of January, then ending February 2026 at 8.91%, to 9.06% as of March 27th 2026 and then reaching 9.27% as of May 1st 2026.

Now, with data for most of May available, Plenum Investments has reported that the overall yield coupon of the catastrophe bond market has risen another 1.6% to reach 9.42% as of May 29th 2026.

Year-on-year the total cat bond market yield metric of 9.42% is now almost 14% lower than it was a year ago, but it has increased and the total return yield or coupon now sits nearly 10% higher than where it fell to early last December, which was its most recent historical low.

Analyse catastrophe bond market yields over time using this chart.

The insurance risk spread, or discount margin, of the catastrophe bond market remains the most important and most changeable factor, being driven by expected seasonal widening effects as the US hurricane season approaches.

The discount margin continues to increase at a slightly faster pace than overall cat bond total returns, or yield coupons. It now stands almost 11% higher over the course of 2026 so far.

The insurance risk spread, or discount margin of the catastrophe bond market had fallen to as low as 4.88% as recently as late November 2025. But steady increases and the re-emergence of seasonal widening lifted risk spreads to 5.72% by May 20t9h 2026.

All of which has been driven by the expected seasonality of cat bond returns, as well as market forces.

Where market forces come into play is in the reduction in cat bond spreads for new issuance, which is factoring into lower overall spreads and returns in the market, as softening of reinsurance drives inevitable lower cat bond pricing at issuance.

Plenum Investments commented on cat bond market yield dynamics through May 2026, “Similar to the previous month, spreads are continuing to widen, with the average market spread increasing by 2% compared to the previous month.

“Comparing the current average spread of 5.72% with the value of 6.59% of a year ago, this 13% reduction in spread suggests a continuation of the market softening. We expect the spread widening to continue moderately through July before the trend reverses, as the hurricane season will then be in full swing.”

As of May 29th 2026, the risk-free return on collateral (based on the money market rate) rose slightly to 3.70% (up from 3.66% at May 1st), while the expected loss of the cat bond market, as measured using Plenum Investment’s methodology, rose slightly to 2.39% (up from 2.38%).

Because of that, the yield (including the risk free rate) over the expected loss of the cat bond market rose to 7.03% at May 29th 2026, which is now up by almost 8.7% over the course of this year so far.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.