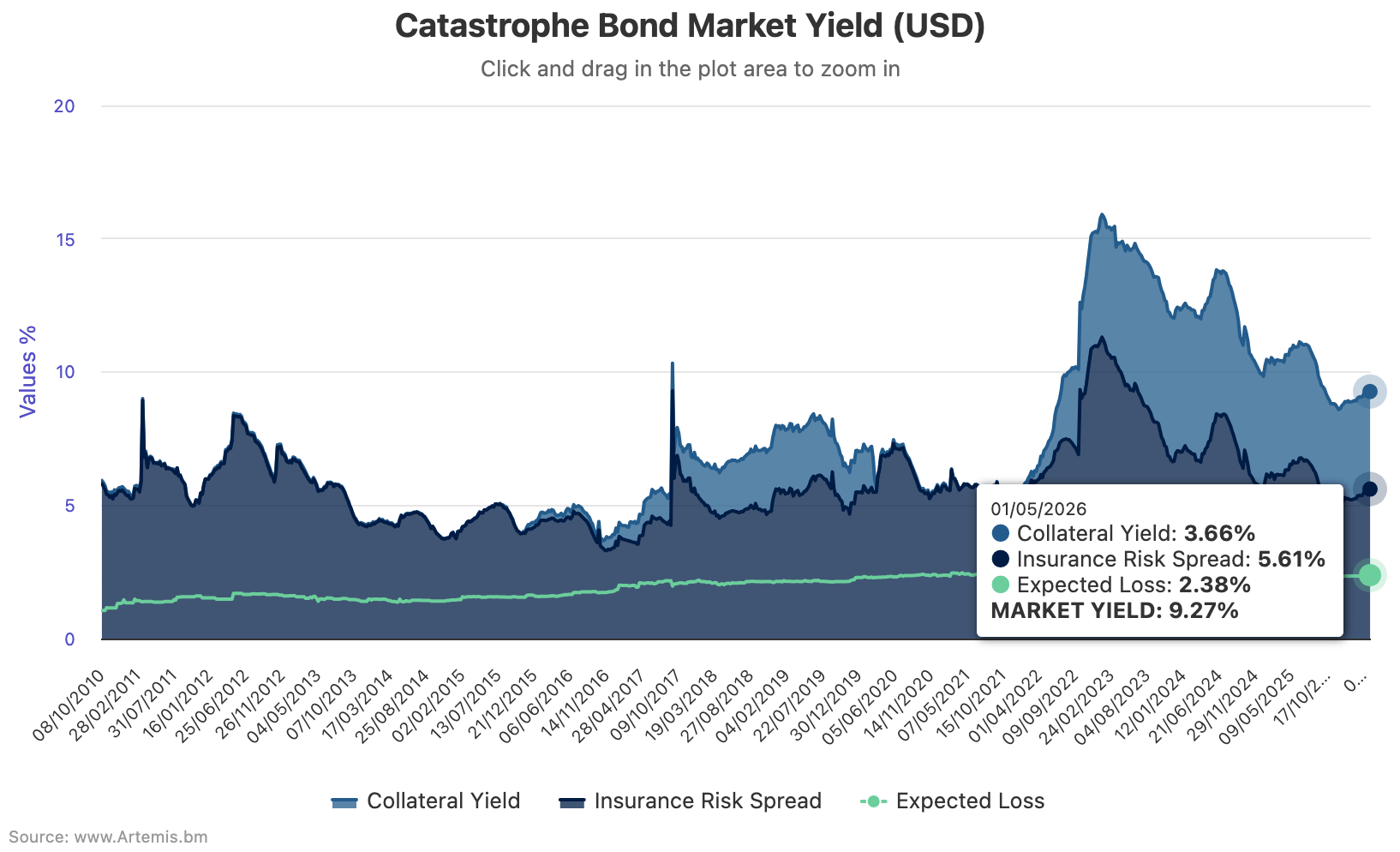

Catastrophe bond market yields rose again through the month of April 2026, as seasonal spread widening effects lifted total returns to almost 9.3%, reducing the year-on year decline in cat bond market coupon to 11% by May 1st, the latest data from Plenum Investments shows.

Cat bond risk spreads began moving slowly higher in February, with the trend continuing in March and accelerating slightly during April.

Cat bond market yield coupons have been steadily rising through 2026 due to relatively slow-paced spread widening, having stood at around 8.80% at the end of December 2025, then rising to 8.87% by the end of January, then again to end February 2026 at 8.91% and through the last month of the first-quarter reaching 9.06% as of March 27th 2026.

Through the next just over one month, to May 1st 2026, the overall yield coupon of the catastrophe bond market has risen another 2.3% to reach 9.27%.

As a result, the cat bond market yield coupon is now up by over 5.3% in 2026 so far. This has helped to reduce the year-on-year decline caused by the softening of prices in cat bonds and reinsurance, having been down almost 15% Y-o-Y at the end of February, then 13% down by March 27th and now only 11% down by May 1st.

The all-important insurance risk spread, or discount margin, of the catastrophe bond market is the key factor, being driven by expected seasonal widening effects as the US hurricane season approaches.

The discount margin has risen faster than overall cat bond total returns, or yield coupons, being now up by 8.5% over the course of 2026 so far.

Plenum Investments commented on cat bond market yield dynamics through April, “Total returns in the CAT bond market varied by currency, ranging from 9.3% (previous month: 9.1%) in USD, to 7.8% in EUR (previous month: 7.5%), and 5.6% in CHF (previous month: 5.3%).

“The average market yield continues to widen, with an increase of 4.4% compared to the previous month. On a year-on-year basis, yields have declined by around 11.3%, indicating a continued softening of the market.

“Regardless of this premium compression, we expect the seasonal spread widening to continue until the start of the hurricane season in June.”

As we’ve reported, the insurance risk spread, or discount margin, of the catastrophe bond market fell to as low as 4.88% at November 28th 2025, but then rose 6% to reach 5.17% by December 26th 2025, rising again to 5.21% by the end of January, to 5.25% by February 27th and to 5.37% by March 27th 2026.

The risk interest spread of the cat bond market has now jumped to 5.61% by May 1st 2026.

At May 1st 2026, the risk-free return on collateral (based on the money market rate) fell slightly to 3.66% (down from 3.69% at March 27th), while the expected loss of the cat bond market, as measured using Plenum Investment’s methodology, rose slightly to 2.38% (up from 2.33%).

Because of that, the yield (including the risk free rate) over expected loss of the cat bond market rose to 6.89% at May 1st 2026, which is now up by 6.5% over the course of this year so far.

The catastrophe bond market is being driven by typical seasonal factors at this time, with the weight of capital and investor interest seemingly less of a drag thanks to the ongoing high levels of issuance, which are helping to keep the market more balanced at this time.

There are still around $4.9 billion of catastrophe bond risk capital from scheduled maturities to come before this quarter is over, so it will be interesting to see if that liquidity in the market suppresses the seasonality to a degree over the next two months.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.