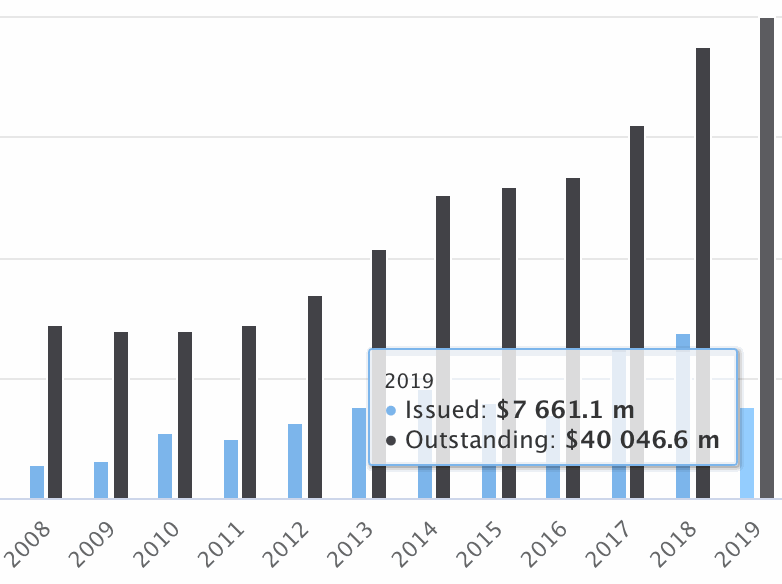

The outstanding market for catastrophe bonds and related insurance-linked securities (ILS) has grown significantly in 2019 so far, passing $40 billion for the first time according to our data, as interest in mortgage ILS offset slower natural catastrophe bond issuance.

It’s a milestone worth celebrating for the insurance-linked securities (ILS) market, as risk capital outstanding reached a new high of over $40 billion this month, with the pool of insurance-linked investment opportunities and use of the cat bond structure expanding all the time.

It’s a milestone worth celebrating for the insurance-linked securities (ILS) market, as risk capital outstanding reached a new high of over $40 billion this month, with the pool of insurance-linked investment opportunities and use of the cat bond structure expanding all the time.

Issuance of mortgage insurance-linked securities (ILS), where mortgage insurers securitize their policy risks and transfer them to the capital market to source reinsurance protection for their books, has helped dramatically.

In fact, it is largely mortgage ILS that has contributed the growth needed to take our measure of catastrophe bond and related ILS risk capital outstanding, based on the transactions recorded in the Artemis Deal Directory, to this new high.

In reaching the almost $40.1 billion of risk capital outstanding figure, the cat bond and related ILS market has grown by an impressive near 7% over the course of 2019 so far (click the chart below to analyse the data) and up around 12% in the last year.

So far in 2019 we’ve recorded over $7.7 billion of issuance, across 144a catastrophe bonds, private cat bond lite deals and the mortgage ILS transactions.

But within that 2019 issuance figure, the mortgage insurance-linked notes or mortgage insurance-linked securities (ILS) deals have accounted for almost half, at $3.675 billion year-to-date.

The other $4 billion or so is made of up of full Rule 144a catastrophe bonds and other property related cat bond lite or private ILS deals.

While $4 billion is far below the issuance levels seen by this stage of the year in the last few, it’s still impressive, we feel, given the catastrophe loss impacts faced by the market and the general reinsurance re-pricing that has been going on.

Mortgage insurance-linked securities (ILS) currently make up 13% of the outstanding market, according to Artemis’ data (analyse the data here).

For full details of catastrophe bond and related insurance-linked securities (ILS) market issuance every quarter please visit our quarterly cat bond market report archive and download them all.

Don’t forget to check out our Cat Bond Market Dashboard as well, for a snapshot of the ILS market, and our range of catastrophe bond market charts and data visualisationswhich allow you to analyse the outstanding market in more detail.

Don’t forget to check out our Cat Bond Market Dashboard as well, for a snapshot of the ILS market, and our range of catastrophe bond market charts and data visualisationswhich allow you to analyse the outstanding market in more detail.

Note: Artemis’ data on catastrophe bond issuance includes every transaction we can source information on, including private deals, new diversifying insurance perils, and the usual 144A broadly marketed property catastrophe issues.

Hence our figures are typically higher than those quoted by reinsurance broker reports, but we feel this offers a holistic look at market activity and use of the ILS or cat bond structure.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.