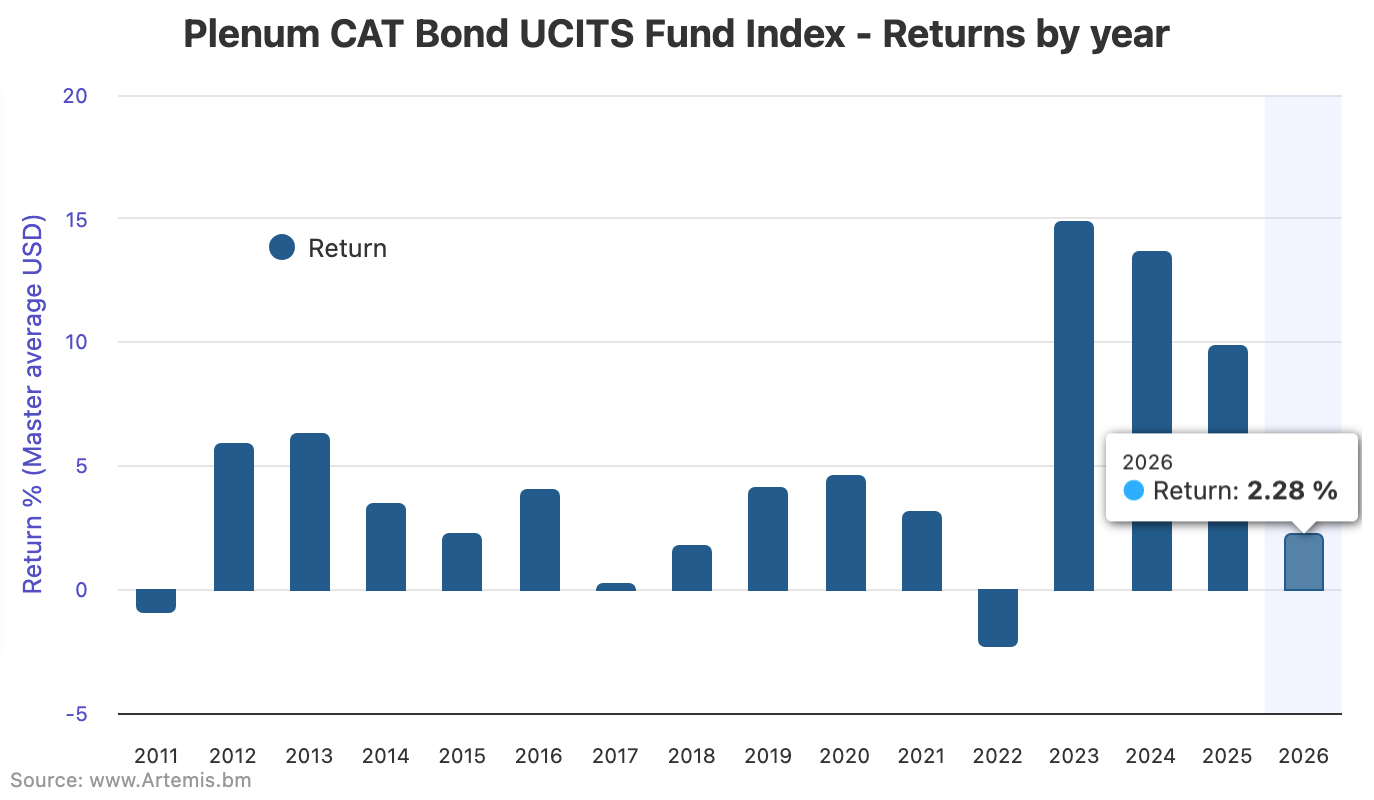

UCITS catastrophe bond funds delivered an average return of 0.36% through the month of May, taking the year-to-date 2026 return through May 29th to 2.28%, while rolling twelve month performance declined slightly to 10.18%, according to the latest data from the Plenum CAT Bond UCITS Fund Indices.

Through the period of May 1st to May 29th 2026, UCITS catastrophe bond funds as a group saw returns averaging 0.36% across all the strategies in this format.

Positive returns and premium accrual continue in the catastrophe bond market, as again there were no major natural catastrophe loss events impacting the investment instruments over recent weeks.

On the back of another positive month, the average year-to-date performance of the UCITS format catastrophe bond fund strategies rose from 1.91% at May 1st to now 2.18% as of May 29th 2026, the latest data available.

The rolling twelve month return across the strategies dipped slightly from 10.37% at May 1st 2026, to come in at an average return of 10.18% at May 29th, still maintaining a double-digit level of performance on this basis for investors.

You can analyse the Plenum CAT Bond UCITS Fund Indices in our charts:

Higher-risk catastrophe bond funds in the UCITS format performed best through the data from May, maintaining their lead on a twelve month basis.

The lower-risk cohort of UCITS cat bond funds delivered an average return of 0.24% for the period May 1st to May 29th inclusive, while the higher-risk cat bond fund strategies averaged a 0.42% return.

Year-to-date, the lower-risk UCITS cat bond funds now average 2.11% so far in 2026, while the higher-risk funds average 2.36%.

On a 12-month rolling return basis, the lower-risk UCITS cat bond funds now average 9.92%, dipping back below the double-digit level again. For the higher-risk cat bond fund strategies, the rolling twelve month return stands at 10.42%.

On a capital weighted basis, the Plenum Index delivered 0.34% for May, 2.28% YTD and 10.44% on a 12-month basis.

Comparing to this time last year, the UCITS cat bond funds had averaged a 2.34% return for 2025 to May 30th, so not that far ahead of 2026’s run-rate so far.

The 12-month return at that time stood at 12% though, so higher than the level seen today. Clearly, lower cat bond pricing at issuance and how that feeds into returns is the main driver of the reduction in the performance of this Index.

We suspect the 12-month return will continue to slowly decline, while soft reinsurance market conditions persist and the stock of catastrophe bonds with lower pricing increases over-time.

But, the catastrophe bond asset class continues to deliver performance deemed highly attractive by investors seeking out relatively uncorrelated sources of return, so appetites to invest are likely to prove persistent.

Analyse UCITS cat bond fund performance, using the Plenum CAT Bond UCITS Fund Indices.

Analyse UCITS catastrophe bond fund assets under management using our charts here.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.