Insurance-linked securities investment fund strategies, across catastrophe bonds and private ILS, delivered an average return of 0.53% for the month of April 2026, according to the ILS Advisers Fund Index which saw all tracked strategies reporting so far as positive for the month.

The 0.53% return for April 2026 is based on only 76% of ILS funds having reported their performance for the month so far and with all ILS fund strategies positive for the month, there is a strong chance the total rises.

The 0.53% return for April 2026 is based on only 76% of ILS funds having reported their performance for the month so far and with all ILS fund strategies positive for the month, there is a strong chance the total rises.

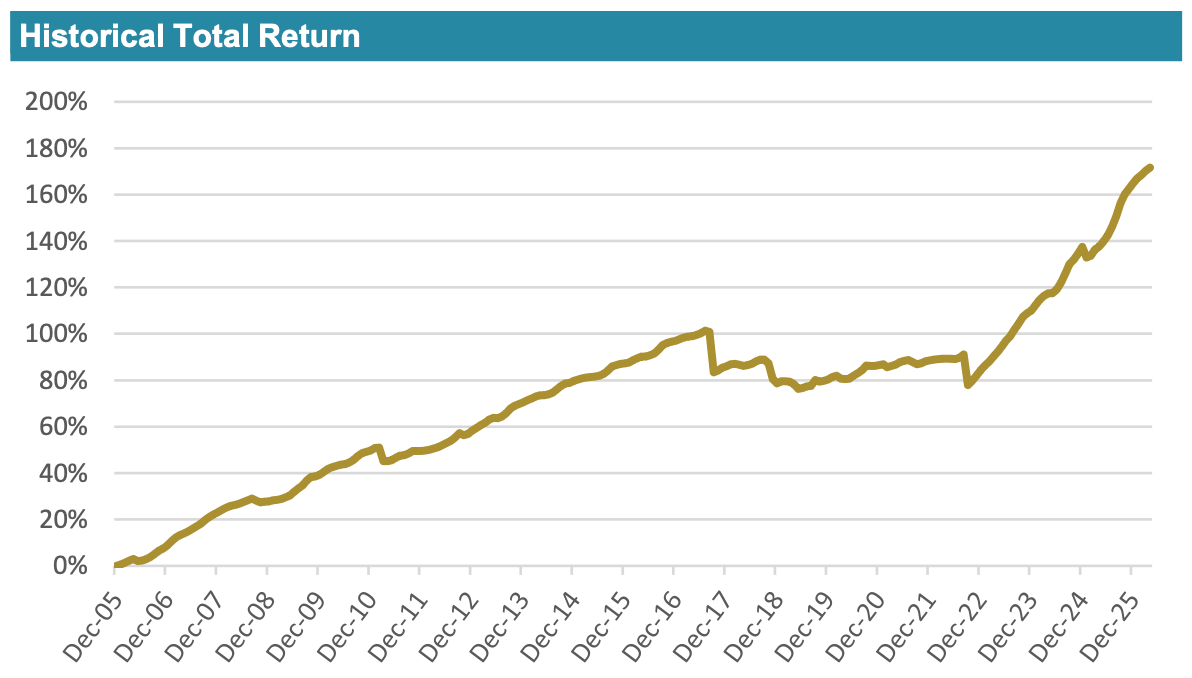

At this stage the average return across the 37 ILS fund strategies that ILS Advisers tracks is now standing at 2.59% for 2026 to the end of April, again a figure that may rise as the remaining ILS investment fund managers report their performance.

Recall that, for the first-quarter of 2026, the average return across ILS funds tracked by the ILS Advisers Fund Index had reached 2.05%.

The second-quarter began with cat bond funds and private ILS fund strategies continuing to demonstrate the benefits of relatively uncorrelated returns for their investors, with another positive month despite ongoing global geopolitical and macro upheavals.

No major catastrophe loss events were reported again in April 2026, helping funds to continue their positive carry momentum and resulting in the current average return of 0.53% for the month.

ILS Advisers noted that spread levels appear to have roughly stabilised at this time, around or close to historical average levels it seems.

The investment manager explained, “Insurance spreads in the cat bond market have stabilized around their long-term averages. At the same time, cat bonds continue to offer spreads well above those of high-yield bonds, supporting sustained investor interest.

“Their low correlation with broader financial markets and geopolitical volatility remains a key attraction, helping to keep supply and demand broadly in balance.”

In April 2026, pure catastrophe bond funds delivered an average return of 0.49% for the month.

Meanwhile, private ILS fund strategies that also invest in collateralized reinsurance and retrocession instruments performed more strongly, with an average return across the group of 0.64%.

All of the ILS funds that have reported their performance so far were positive for the month, while the range between best and worst so far stands at between 0.33% and 0.93%.

Track the ILS Advisers Fund Index here on Artemis.

You can track the ILS Advisers Fund Index here on Artemis. It comprises an equally weighted index of 37 constituent insurance-linked investment funds which tracks their performance and is the first benchmark that allows a comparison between different insurance-linked securities fund managers in the ILS, reinsurance-linked and catastrophe bond investment space.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.