Insurance-linked securities (ILS) portfolios with predominantly catastrophe bond holdings have on average outperformed many mid- and higher-risk ILS fund strategies that contain private ILS transactions over recent years, according to analysis from Frontier Advisors.

Catastrophe bonds typically provide reinsurance or retrocessional protection higher up in the risk tower, so are more risk-remote and so the cat bond market tends to only be significantly impacted by really major catastrophe loss events.

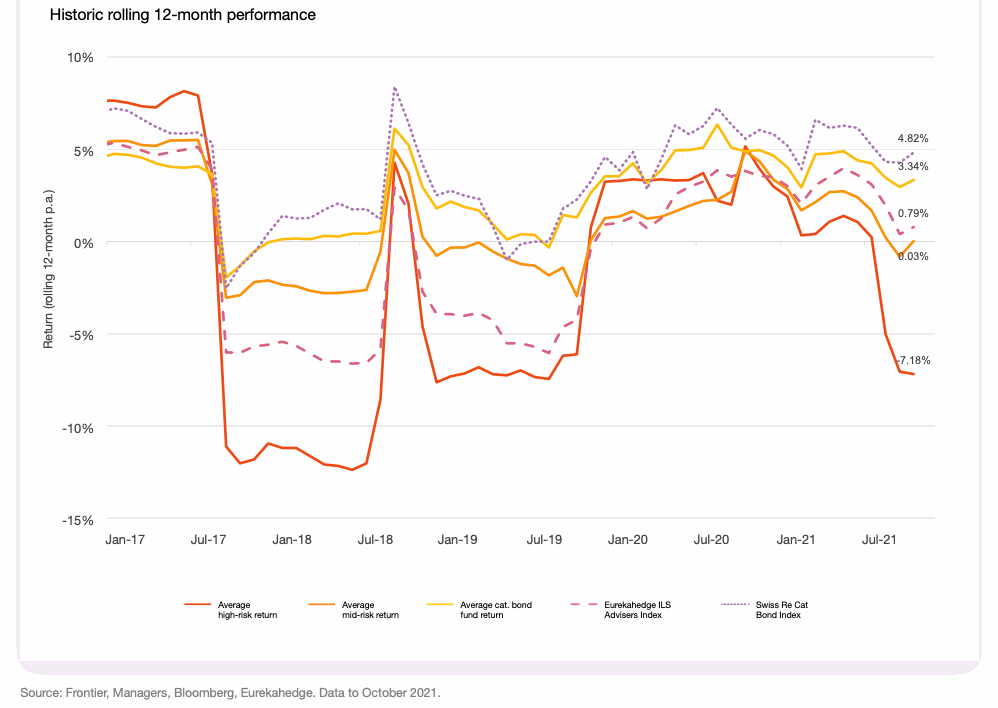

Given the catastrophe and severe weather loss environment since 2017, Frontier Advisors, an Australian independent investment consultant with an insurance-linked securities (ILS) specialism, believes that catastrophe bond funds have historically outperformed private ILS funds since 2017 and 2018.

The chart below shows that both the accepted benchmark index for the catastrophe bond market from Swiss Re and the average cat bond fund return have outpaced the average return of private ILS strategies on a rolling twelve month basis in recent years.

The frequency of loss events that affected the collateralised reinsurance and retro market has been higher in recent years, while ILS capital has moved into layers that were more readily impacted by the kind of loss activity seen.

Frontier believes a number of factors stand out as driving the outperformance for catastrophe bond fund strategies.

First, the fact private ILS fund strategies hold more risky positions in the insurance capital structure, compared to catastrophe bonds, which of course means private ILS contracts are often more exposed when loss activity occurs.

But, perhaps more importantly over the last few years, the private ILS fund portfolios tend to hold more aggregate exposure, as well as more diversified portfolios, meaning they are often exposed to smaller loss events, as well as loss events in parts of the world or for perils where catastrophe bonds are not in use.

The other main factor driving the underperformance of average private ILS fund returns, versus cat bond funds, is the impacts of loss creep.

Loss creep has persistently affected some private ILS funds from the 2017 and 2018 catastrophe years, with some impacts even in the second-half of 2021 due to increasingly ultimate net loss estimates from ceding companies.

Loss creep has proved to be a drag on private ILS funds in recent years, driven by the complexity of certain events in 2017 and 2018.

Although it is important to consider how inaccurate early estimates were from some ceding companies, as well as the social inflationary factors that served to drive a lot of loss creep from this period.

While catastrophe bond funds have now outperformed mid- and high-risk ILS fund strategies over a one, three and five year time horizon, according to Frontier Advisors, it is still true that some cat bond fund strategies can suffer more severe losses from single major catastrophe losses, given their greater concentrations to peak peril exposures.

The chart below from Frontier Advisors shows the spread of cat bond fund performance vs mid- and high-risk, more private ILS focused fund strategies.

Comparing 2020, when reinsurance market losses from catastrophes were still high, there was very little cat bond impairment. But 2021 saw a significant number of events earlier in the year, impairing more cat bonds according to Frontier Advisors analysis.

In fact, with catastrophe losses remaining high through 2021, Frontier said more cat bonds were impaired in 2021 than in 2019 and 2020 combined.

But still the performance of catastrophe bond weighted ILS funds has outperformed many private ILS focused strategies.

We should add here that there are lower-volatility private ILS strategies that did remarkably well in 2021, as their exposure to individual events was lower and their aggregate exposure in some cases negligible.

Portfolio strategy appears to have been key in defining how profitable ILS fund strategies have been over the last few years, with the way collateralized reinsurance and retrocession became increasingly aggregate focused through the high-growth years of the ILS market, as well as the expansion of the collateralized retro market both key factors in the lower performance of many private ILS fund strategies, it seems.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.