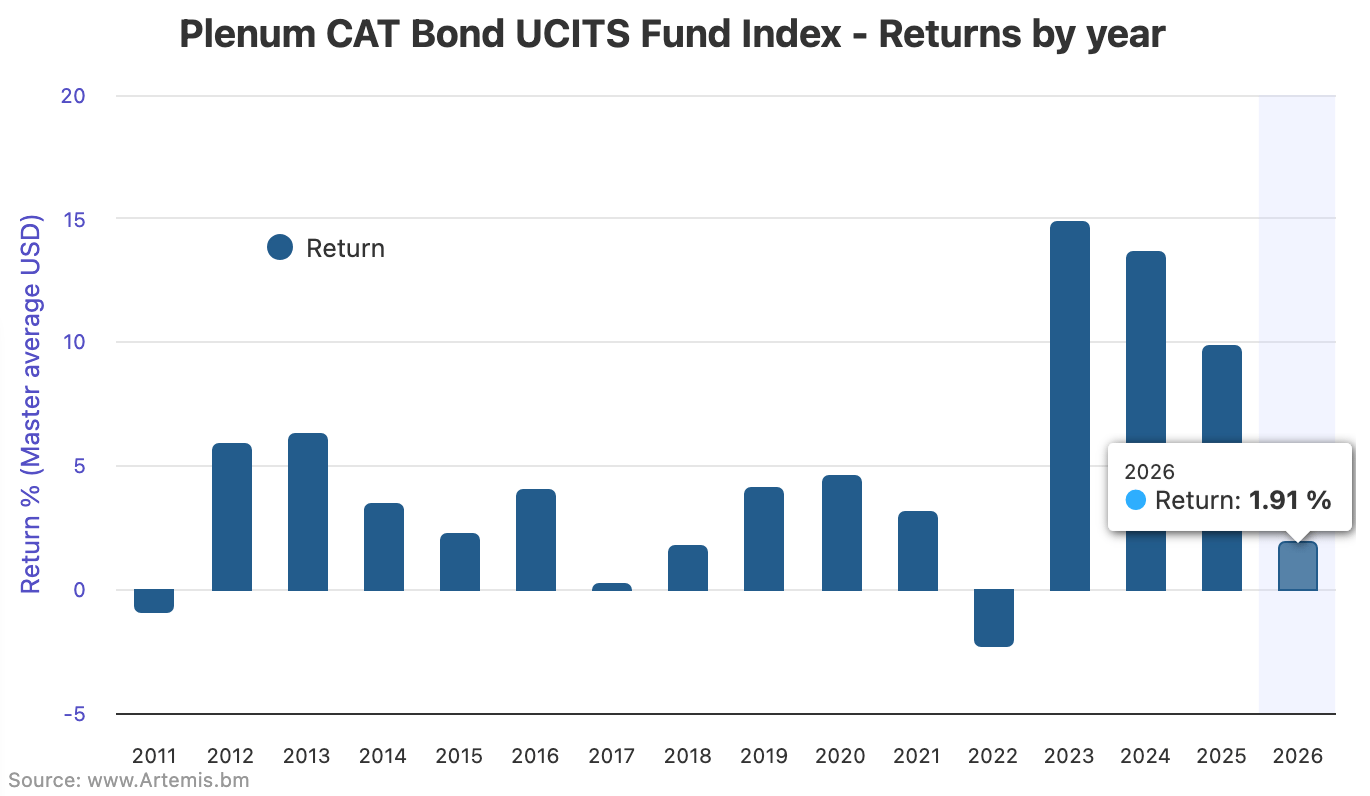

UCITS catastrophe bond funds currently stand at an average return for 2026 through May 1st of 1.91%, while their performance over the last twelve months stands at an average return of 10.37%, according to the latest data from the Plenum CAT Bond UCITS Fund Indices.

Catastrophe bond funds in the UCITS format returned 0.55% on average through the period of March 27th 2026 to May 1st 2026, the latest data available.

That was a slightly better performance than the previous monthly data, which saw these cat bond funds returning 0.35% on average through the period of February 27th to March 27th 2026.

As a result, the average year-to-date performance of these cat bond fund strategies in the UCITS format rose from 1.35% at March 27th to now 1.91% as of May 1st 2026.

With the latest period again seeing no major loss activity, it is expected all UCITS cat bond funds will have been positive again.

On a rolling twelve month return basis, the total now stands at 10.37% at May 1st 2026, which is actually a slight increase from the 10.23% that the twelve month return stood at as of March 27th.

You can analyse the Plenum CAT Bond UCITS Fund Indices in our charts:

Over the last month or so of data that is available, the lower-risk cohort of UCITS cat bond funds actually outperformed the higher-risk group of strategies.

The low-risk cohort of UCITS cat bond funds delivered an average return of 0.65% for the period March 27th to May 1st inclusive, while the higher-risk group of cat bond strategies averaged a 0.51% return.

It takes the average performance year-to-date through May 1st for the lower-risk cat bond funds to a 1.86% return, while the higher-risk funds stand at 1.94%.

For the lower-risk UCITS cat bond funds the 12-month return now stands at 10.27%, while the higher-risk cat bond funds stand at an average return of 10.50%, with both those figures slightly up from the 12-month return a month ago.

Spread widening may be the reason for the slight increase in the average 12-month returns for these cat bond fund categories, however it may also be year-on-year differences as 2025 saw some recovery in value through the second quarter after certain California wildfire loss exposures became clearer.

It will be interesting to see how seasonal spread widening affects performance over the coming months, as long as the catastrophe bond market remains free of major loss impacts.

Analyse UCITS cat bond fund performance, using the Plenum CAT Bond UCITS Fund Indices.

Analyse UCITS catastrophe bond fund assets under management using our charts here.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.