Global reinsurance company Swiss Re expects that property and casualty (P&C) insurance premiums will grow considerably over the next two decades, with a near doubling expected. Climate risk will be a major driver of this, resulting in a significant boost to new property P&C premiums written, but also to expected insured natural catastrophe losses.

Overall, the P&C insurance risk pool is expected to increase by around two times, to roughly US $4.3 trillion of premiums by 2040.

But, of note to reinsurance and insurance-linked securities (ILS) markets, the global P&C risk pool is expected to become riskier and more complex at the same time, Swiss Re explained in its latest sigma report that was released today.

Emerging markets will rise fastest, resulting in a gain in share, from 20% of P&C risk pool premiums in 2020 to 33% in 2040.

Climate change and climate risk is going to be one of the biggest drivers of insured property premiums in the P&C space, with property expected to be one of the biggest drivers of growth in global insurance and reinsurance markets over the coming years.

Climate change and climate risk is expected to add $183 billion of new P&C premiums globally by 2040, according to Dr. Jérôme Haegeli, Group Chief Economist of Swiss Re, who was speaking at a launch event for the sigma report today.

Today, some roughly 25% of P&C insurance premiums are related to property lines of business, but by 2040 this is expected to rise to 29% of the overall P&C risk pool premiums.

That equates to an expectation that property insurance premiums could almost triple by 2040, adding some $1.3tn more in premiums by that stage.

Haegeli said that economic growth is the main driver, explaining about two-thirds of this increase in premiums.

Specifically on the climate risk front, Swiss Re expects the property risk pool to increase in size by 30% to 40% on the back of rising climate exposures.

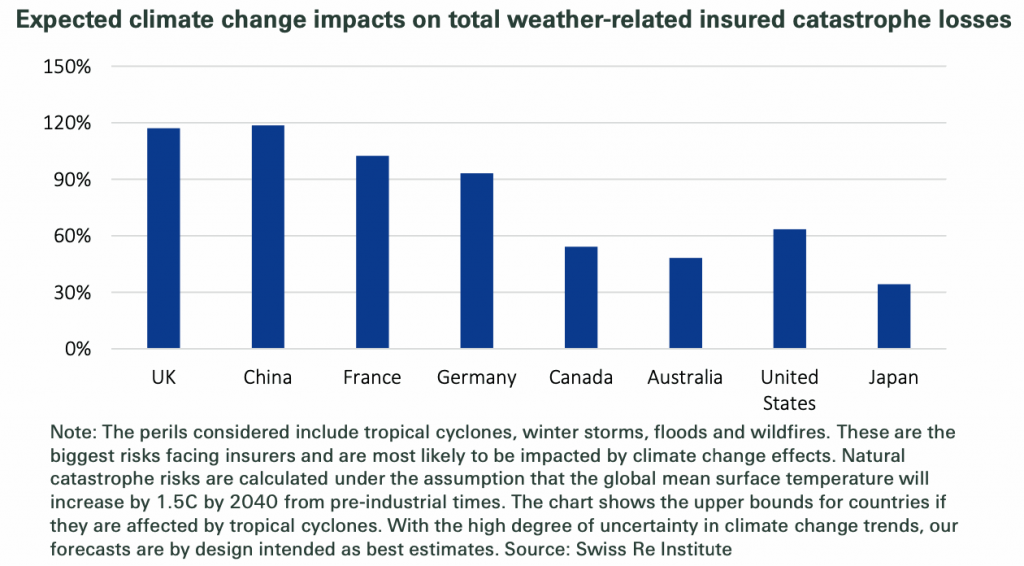

The result of this is an expectation that insured catastrophe losses will rise significantly, with Swiss Re estimating that weather related insured catastrophe losses will increase by between 30% to 63% in key advanced markets by 2040.

The main drivers are expected to be floods, tropical cyclones and perils like wildfires.

While the increase of up 63% is significant, it is expected to be even bigger for some key insurance and reinsurance markets, with locations like Germany, China, France and UK expected to see a 90% to 120% increase in insured catastrophe losses by 2040.

All of this will translate into significant opportunity for those able to create and structure relevant insurance and reinsurance products to provide cover to property as climate risks increase.

While there will also be a growing need for risk capital to underpin this, suggesting more opportunity for the reinsurance and insurance-linked securities (ILS) markets.

Swiss Re highlighted the, “Increasing need for reinsurance due to more severe catastrophe losses,” but also highlighted the increasing uncertainty in losses, in particular from so-called secondary perils.

This means risk-adjusted price adequacy is going to be critical as the property premium risk pool is enlarged by climate change related risks.

The P&C insurance and reinsurance industry is going to find its premium base increasingly driven towards more complex risks, in the property and liability space, while lower volatility drivers of the past, such as motor, will be less of a contributor.

Over time, if climate risks continue to escalate, property could become the biggest component of the P&C insurance and reinsurance risk pool, suggesting ongoing need to innovate in provision of efficient risk capital that can support this rapid expansion.

Jerome Haegeli, Swiss Re’s Group Chief Economist, commented “Promoting the conditions for long-term sustainable growth is particularly important in the face of climate change, which poses the biggest long-term threat to the global economy. If we are to build a sustainable insurance system that allows society to manage and absorb future risks, we need to make risks and opportunities quantifiable. Our work is also vital for policy makers with whom we share the aim of making economic growth insurable.”

Gianfranco Lot, Head Globals Reinsurance at Swiss Re, added, “With the global portfolio shifting from lower risk motor insurance to higher risk lines, P&C insurance business will become more volatile. At the same time, risk modelling will become more complex, which will lead to higher capital requirements and an increased demand for reinsurance. In this fundamentally different risk environment, reinsurers will play a crucial role in keeping risks insurable.“

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.