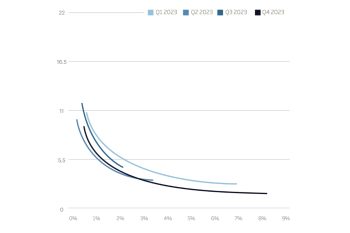

Cat bond investors secured higher risk-adjusted returns in 2023 as multiple rises

12th April 2024While the pricing of cat bond notes stabilised somewhat in the final quarter of 2023, persistently firm reinsurance and retrocession rates saw investors achieve higher risk-adjusted pricing throughout the year, according to Artemis’ data.

Read the full article