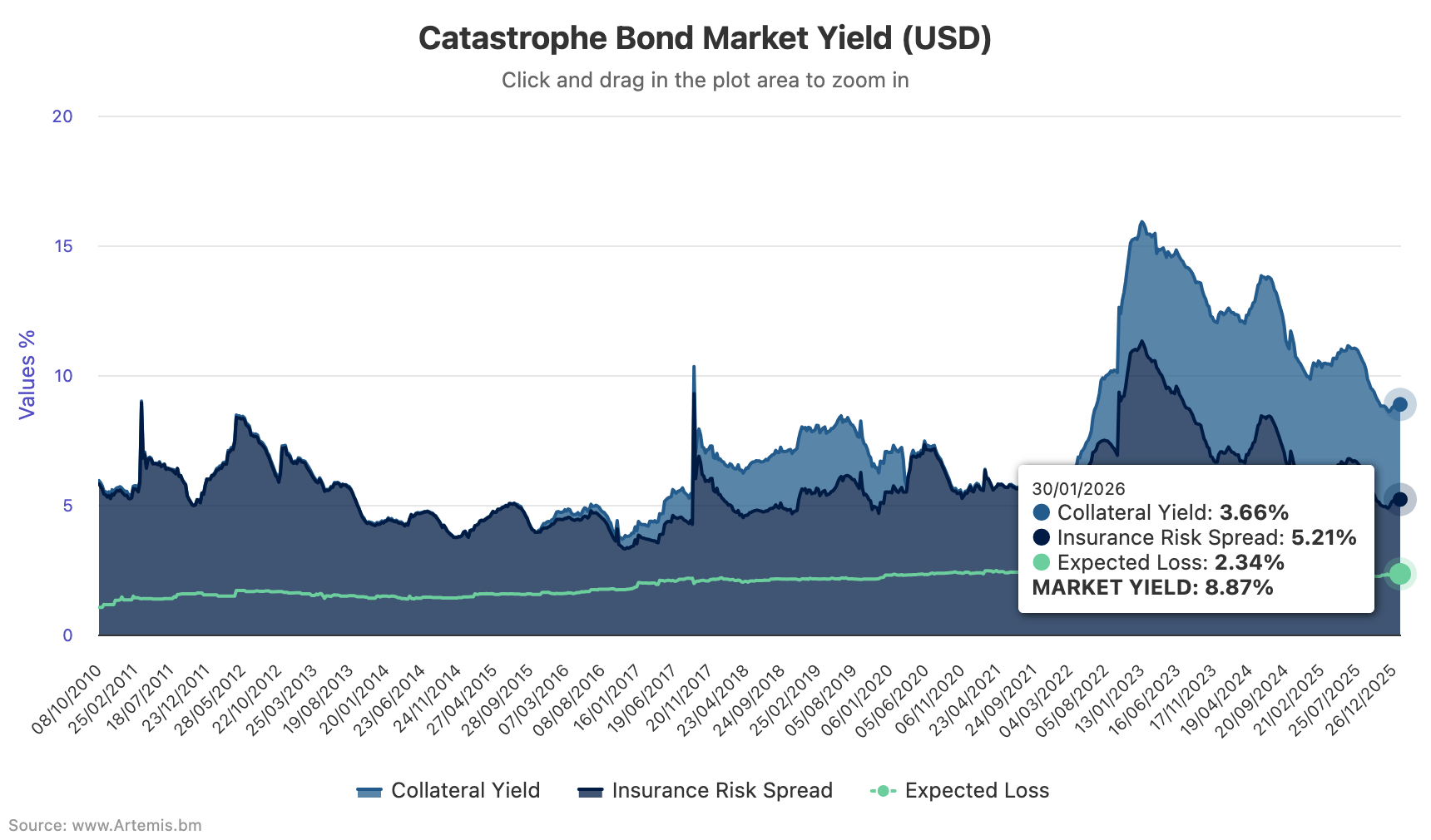

Catastrophe bond market insurance risk spreads, or the discount margin, did not rise as much as anticipated in the month of January 2026, as demand moderated widening and the overall yield of the catastrophe bond market ended the month only slightly higher at 8.87%, data from Plenum Investments shows.

Which was only a slight increase on the 8.80% yield the catastrophe bond market offered as of the end of 2025, after December saw a return of spread widening trends.

Seasonal spread tightening related to the cat bond market’s peak peril, the Atlantic hurricane season, had compressed catastrophe bond market spreads through the second-half of 2025, a trend that began to slow in November as the wind season drew to its close for the year.

December 2025 then saw cat bond market insurance risk spreads, or the discount margin, increase by roughly 6% in the month, to the aforementioned 8.80%.

But then January 2026 only saw the slight rise as the cat bond market yield remained relatively flat month-on-month, reaching January 30th at 8.87%, which Plenum Investments noted was due to continued high investor demand in the marketplace.

Plenum Investments commented on developments in the coupon of the cat bond market in January 2026, explaining, “In January, spreads did not widen as usual due to a still slightly higher level of demand. By the end of January, the average USD insurance yield reached 5.2%.”

Adding that, “We expect it to exceed the 10-year average again in the near future, as it continues to follow its typical upward trend.”

The insurance risk spread, or discount margin of the catastrophe bond market, had declined to as low as 4.88% at November 28th 2025 on the back of seasonal spread tightening.

It had risen 6% to reach 5.17% by December 26th 2025. But in January 2026 only managed to rise a further 0.8% to end the month at 5.21%.

The risk-free return on collateral had been shrinking, falling to as low as 3.63% as of December 26th. In January 2026 it rose slightly to end the month at 3.66%.

The expected loss of the cat bond market, as measured using Plenum Investment’s methodology, rose one basis point from 2.33% at December 26th 2025, to 2.34% by the end of January 2026

As a result, the yield over expected loss of the cat bond market including the risk free rate, rose from 6.47% on December 26th 2025 to reach 6.53% as of January 30th 2026.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.