Catastrophe bond issuance for the first-half of 2026 is now projected to reach $16.3 billion according to the latest Artemis Deal Directory data, which could rise further as there remain a number of offerings in the market which could upsize, while further new deals could emerge.

Catastrophe bond issuance in 2026 has continued to accelerate and the addition of State Farm’s new $1.5 billion of Merna Re Enterprise cat bonds yesterday has given issuance a meaningful boost.

Catastrophe bond issuance in 2026 has continued to accelerate and the addition of State Farm’s new $1.5 billion of Merna Re Enterprise cat bonds yesterday has given issuance a meaningful boost.

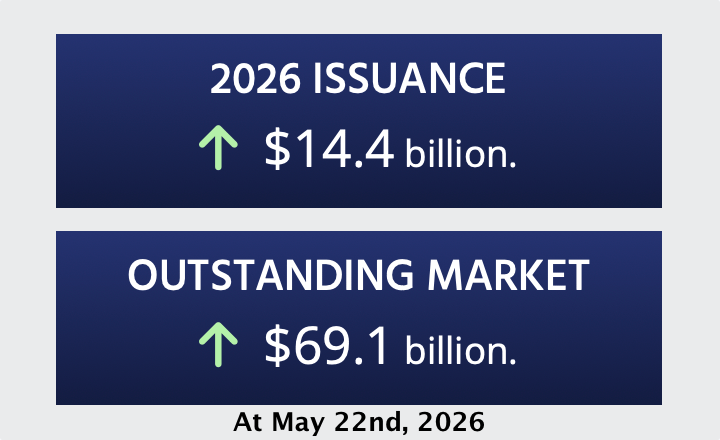

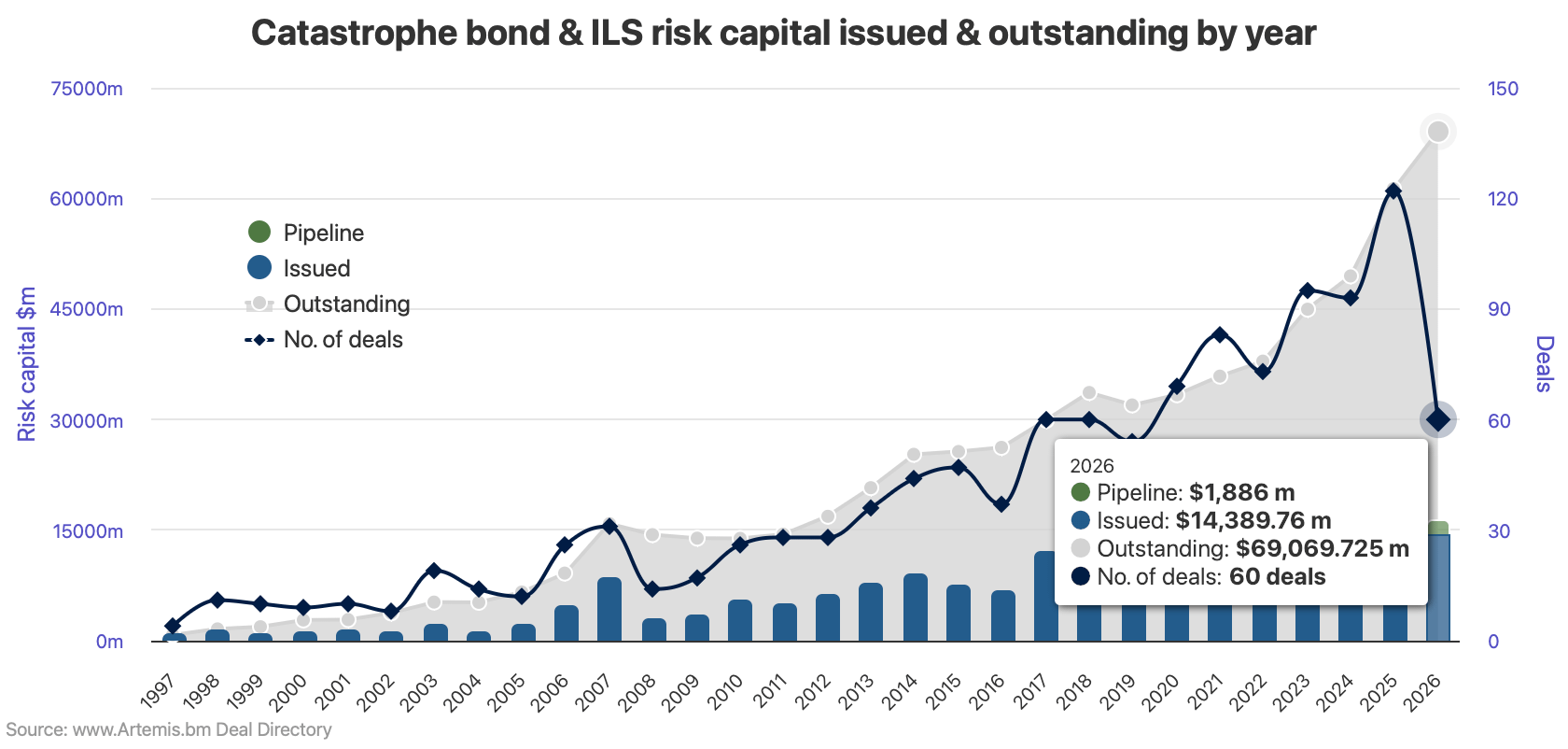

As of today, completed and fully settled issuance of 144A catastrophe bonds and the few private cat bond placements we track in our Deal Directory stands at almost $14.4 billion.

Of that, over $14.1 billion are Rule 144A catastrophe bonds and the rest private issuances we’ve reported on and tracked.

Within the 144A cat bond bucket, over $13.72 billion of issuance settled so far in 2026 are property catastrophe bonds, while only $384.5 million cover specialty or life/health related business.

While issuance is roughly keeping pace with the records set in 2025 so far, there is still a way to go to set a new record of settled cat bond issuance by the end of June 30th.

H1 2025 saw over $17.56 billion of issuance, across 144A and private cat bonds tracked by Artemis.

That comes from 60 settled transactions so far and the current pipeline features another 12 cat bond offerings, so the deal total for the first-half will be at least 72 it seems, which is more than half the total 122 cat bonds we tracked in full-year 2025.

Notably, the outstanding cat bond market by Artemis’ measure has grown by almost 13% so far this year, now standing at $69.1 billion as of today.

Maturities will take that down slightly in June (almost $4.5bn are scheduled), unless the pipeline grows substantially.

Settled cat bond issuance in May 2026 now stands at more than $5.8 billion, which is only the second time this month has surpassed the $5 billion milestone (last year being the first).

In fact, May 2026 is now on-track to become the biggest issuance for that month on-record in 2026, with a number of additional cat bonds still to settle and issuance now projected to be well over $6 billion.

Should additional catastrophe bonds that are currently in the pipeline upsize, or more new deals come to market that settle before the end of June, a new first-half record is still possible at this time.

From the sponsor perspective, the catastrophe bond market continues to execute strongly on price, with ceding companies securing their reinsurance and retrocession at attractive pricing.

With meaningful cash still to come in maturities this June, the market will be able to support additional issuance in the first-half and this should ensure that attractive conditions persist for sponsors through the coming weeks and potentially into the start of the third-quarter as well.

While July is typically a quieter month for new cat bond issuance, given the Atlantic hurricane season is underway at that time, the levels of cash in the market from maturities might make later sponsorship, or sponsorship of cat bonds with diversifying perils, a very good option for insurers and reinsurers this year.

We will continue to update you as the rest of the first-half progresses and alert you to any records that may be set.

Download our free quarterly catastrophe bond market reports.

We track catastrophe bond and related ILS issuance data, the most prolific sponsors in the market, most active structuring and bookrunning banks and brokers, which risk modellers feature in cat bonds most frequently, plus much more.

Find all of our charts and data here, or via the Artemis Dashboard which provides a handy one-page view of cat bond market metrics.

All of these charts and visualisations are updated as soon as a new cat bond issuance is completed, or as older issuances mature.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.