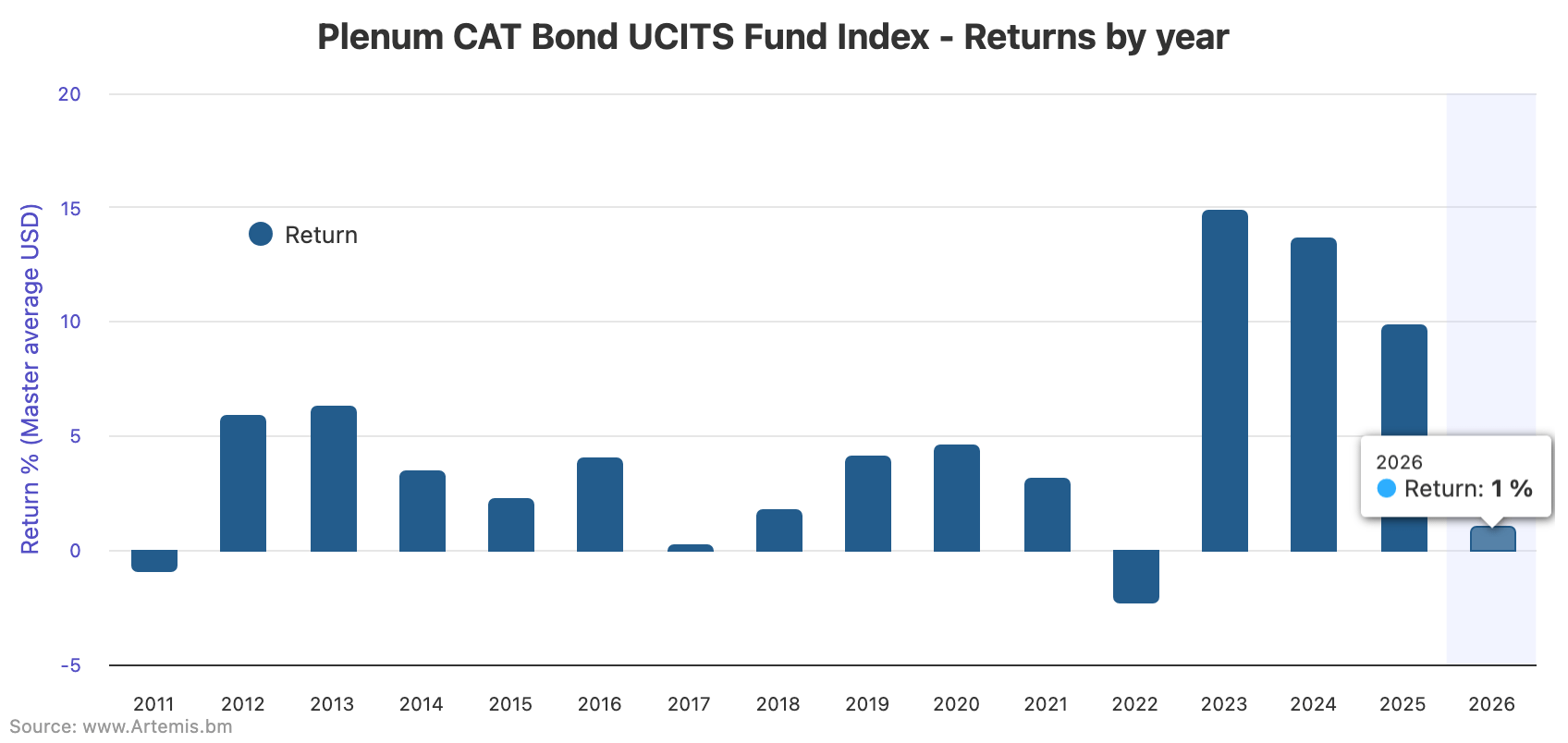

UCITS catastrophe bond fund strategies delivered an average return of 0.46% for February 2026 taking their year-to-date performance to 1.00%, according to the Plenum CAT Bond UCITS Fund Indices.

Last month’s average catastrophe bond fund return has beaten the prior year for the second in a row, with this UCITS cat bond fund index only up 0.32% in February 2025 and the Swiss Re cat bond index having only managed a 0.42% return for that month.

It takes the year-to-date average return across UCITS cat bond funds to now 1%, which is higher than the 0.82% level of performance after February last year.

It’s important to remember that the Los Angeles wildfires dented the start of 2025 though and some of that lost value was recovered through following months, so we do expect the UCITS cat bond fund index to drop behind 2025 over the next quarter.

As a reminder, catastrophe bond fund strategies in the UCITS format began 2026 positively, delivering an average return of 0.53% for January which was above average for the month.

February 2026’s 0.46% average return across the UCITS cat bond funds (up to and including February 27th) is close to the average, while a 1% start for the first two months of the year is above the historical average year-to-date.

All catastrophe bond investment fund strategies are expected to have delivered positive returns for February 2026, given there were no impactful natural catastrophe insured loss events around the world that would have reached the reinsurance layers where cat bonds typically reside.

While there have been some cases where aggregate cat bonds have seen price effects from smaller, typically winter weather related events, these are not significant and have not created any meaningful impacts across portfolios.

You can analyse the Plenum CAT Bond UCITS Fund Indices in our charts:

Plenum Investments’ data shows that higher-risk UCITS catastrophe bond fund strategies outpaced the lower risk group of cat bonds funds during the month.

For the higher-risk UCITS cat bond index the return for February was 0.48%, for lower-risk strategies 0.41%.

Year-to-date, to February 27th, higher-risk UCITS cat bond funds have averaged a 1.06% return, while lower-risk cat bond funds averaged 0.87% for the period.

On a 12-month rolling return basis to February 27th 2026, the average return across the UCITS catastrophe bond funds tracked by this Index now stands at 10.46%, which is actually slightly up on the end of January 12-month return of 10.31%.

For the lower-risk cohort the 12-month return now stands at 10.20% (slightly down on the end of January 10.28%), while for the higher-risk cat bond fund cohort it stands at 10.73% (up on the end of January 10.36% 12-month return).

Catastrophe bond funds continue to benefit from coupon returns to start the year in 2026. It’s expected that the lower spread environment will begin to show in cat bond fund performance as the year progresses, but as ever it will be any major natural catastrophe loss events that occur that could be the main potential detractor to performance.

Analyse UCITS cat bond fund performance, using the Plenum CAT Bond UCITS Fund Indices.

Analyse UCITS catastrophe bond fund assets under management using our charts here.

Analyse catastrophe bond market yields over time using this chart.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.