Diversifying spreads and normalised valuations reshape cat bond market in 2025: Steiger, Icosa

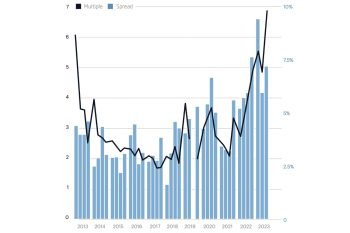

26th January 20262025 saw a long-standing pattern reverse within the catastrophe bond market, as diversifying risks began offering spreads comparable or higher than those of traditional peak perils, while valuations between index-linked and indemnity structures normalised, Florian Steiger, CEO of Icosa Investments AG highlighted in a recent report.

Read the full article