Property catastrophe reinsurance rates softened again at the key January 2019 renewal season, but the retrocession market which saw more loss-affected accounts renew saw double-digit hardening, according to JLT Re.

Capital levels in reinsurance continued to play a significant role at the January 1st 2019 reinsurance renewal season, the broker explained, resulting in a softer market this January than was seen a year ago.

However our sources suggest that much of this fresh softening has been in areas of the market largely dominated by traditional reinsurers (Europe, Asia Pacific, large property accounts), as they continue to deploy capacity at levels that may be unsustainable for some of their more costly business models.

After this renewal, JLT Re says that the reinsurance market is in uncharted territory, as it faces the new normal of more stable pricing and rates.

Expectations had been high for stronger rate increases at January 1st this year, but these expectations have been defied, JLT Re says, as for the second year running rate increases failed to live up to them.

Overall, JLT Re sees pricing as having been broadly stable, with pockets of rate increases in underperforming and loss-affected areas of the marketplace.

Some excess capital has been absorbed “at the margin” the broker notes, but overall reinsurance remains well capitalised which does not bode well for the renewals further into 2019.

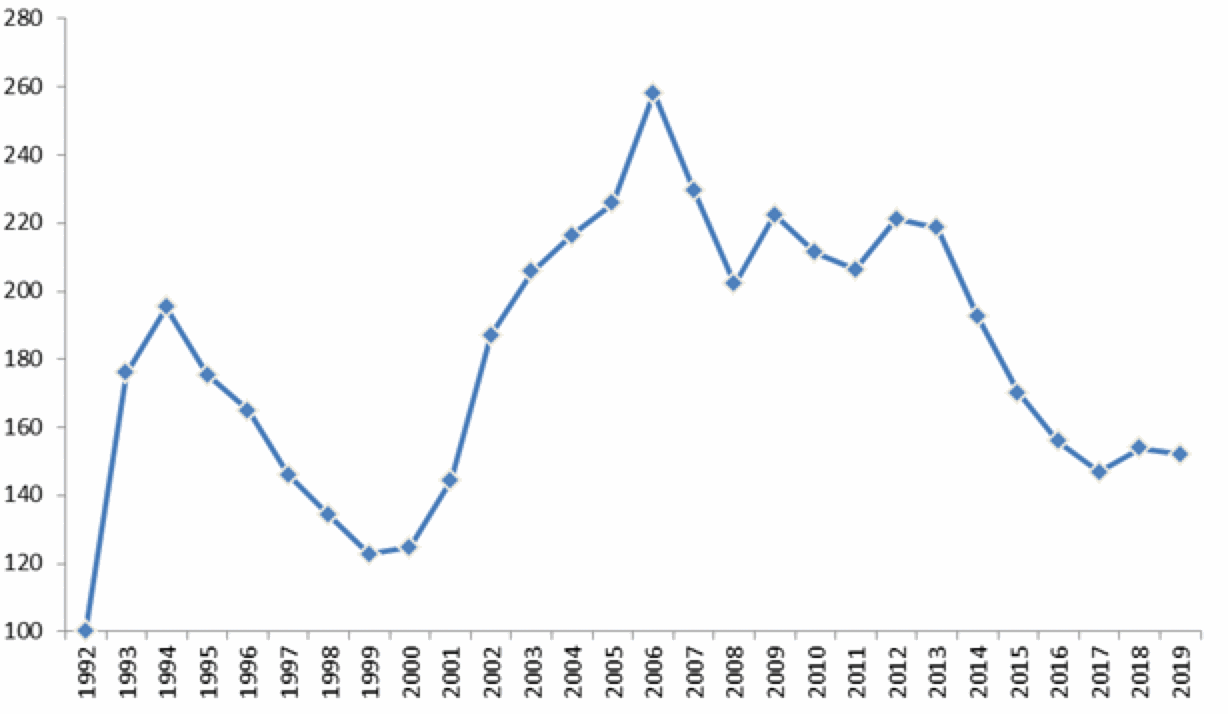

In property catastrophe reinsurance specifically, JLT Re notes that it recorded the market softening at January 1st.

The brokers Risk-Adjusted Global Property-Catastrophe Reinsurance Rate-on-Line (ROL) Index declined by -1.2% at 1st January 2019, which compares to an increase of 4.8% at 1st January 2018.

This will be seen as particularly disappointing, but given the focus of the January renewals it does reflect the renewals across Europe and Asia Pacific excluding Japan, so is perhaps a sign that the more recent losses have not affected the big reinsurance firms as much as the three hurricanes in 2017.

JLT Re Risk-Adjusted Global Property-Catastrophe Reinsurance Rate-on-Line (ROL) Index

After this year’s decline, the Index now sits below levels that were recorded in 2016 and global property-catastrophe pricing now sits approximately 30% below 2013 levels, JLT Re says.

How sustainable these pricing levels are remains to be seen, over the longer-term, but it is certain that only the most efficient or most globally diversified business models could sustain this over years, meaning pressure to lower expenses, raise efficiency, leverage lower-cost capital and to consolidate will remain high among the reinsurers, especially the small to mid-sized players.

Ed Hochberg, Chief Executive Officer, JLT Re in North America, commented, “Despite another active catastrophe year in the United States, property-catastrophe rate changes were modest at 1 January 2019. Loss-free layers saw relatively muted movements, typically falling within a range of flat to down 5%. Strongly performing accounts renewed towards the lower end of this range as cedents argued (often successfully) that another clean year merited risk-adjusted decreases in 2019. Loss-impacted layers generally saw price rises, but outcomes varied depending on losses, geographies, exposures and relationships.”

The retrocession market fared better, with double-digit rate increases seen across loss-affected accounts and dislocated areas of the market.

Capacity constraints dominated this market, JLT Re said, as the effects of trapped collateral from collateralized retrocessionaires played into renewal negotiations.

“The quantum and timing of 2018 catastrophe losses was such that a sizeable portion of retrocession capital, the bulk of which is provided by third-party investors, was trapped for a second consecutive year,” the broker explained.

A reduction in investor appetite and less willingness to add more capital for these renewals also impacted ILS funds and their appetites at the renewals. This helped to support rates in the areas that ILS funds dominate the market, although it does mean ILS market growth has stalled for the first time in a number of years.

JLT Re said, “Investor appetite softened in the fourth quarter, especially when compared to the same period in 2017. Appetite had been moderating throughout 2018 due to lower-than-expected returns and loss deterioration from 2017 events. Many insurance-linked securities (ILS) funds therefore confronted a more challenging environment this renewal.”

The market experienced a challenging period with some redemptions and fundraising was a challenge, the broker notes, resulting in lost or trapped collateral not being replenished to the same degree as in prior years.

But our sources suggest that many ILS funds, while not seeking growth, have been happy with their renewals, becoming increasingly selective and relying on their relationships and access to specific business to fulfill their deployment needs.

As we highlighted earlier, some ILS funds have pulled back from the areas where the most softening has been seen, preferring to avoid areas of the market where major reinsurers are driving the price.

While some ILS funds report being happy with their renewals and feeling that overall the risk adjusted pricing of their portfolios has improved a little, boding well for 2019 returns if catastrophe experience is lighter than the last two years.

While retrocession rates largely increased by double-digits, this market picture was more nuanced, as differences emerged between occurrence and aggregate layers, as well as between ILS markets and traditional reinsurers.

Bradley Maltese, Deputy CEO of UK & Europe, JLT Re, commented on retro and global property markets, “After another year of significant losses and locked capital in the retrocession market, rates for loss-affected catastrophe layers were generally up by between 10% and 20% on a risk-adjusted basis, with aggregate covers falling towards the upper end of this range. Many clean occurrence retrocession programmes were renewed flat to up 10%. Global and Lloyd’s direct and facultative (D&F) catastrophe covers were less affected by 2018 losses and, after strong increases at last year’s 1 January renewal, rate changes in 2019 were typically down 2.5% to down 7.5% on a risk-adjusted basis.”

Overall, capital and capacity continues to drive reinsurance pricing, as well as the appetites of major reinsurers, it seems.

David Flandro, Global Head of Analytics at JLT Re, stated, “Sustained capital inflows have offset mounting pricing pressures to bring relative stability to the reinsurance market over the last several years. Record levels of dedicated sector capital at year-end 2018 once again helped ensure continued, plentiful capacity across most lines at 1 January 2019. A small portion of excess sector capital was nevertheless absorbed in 2018 by sizeable insured catastrophe losses in the second half of year, a reduction in third-party deployable capital, higher demand for reinsurance and a renewed focus on underwriting discipline, as shown, for example, by reduced stamp capacity and higher capital requirements at Lloyd’s.”

At a renewal when ILS markets have contracted a little, overall, it seems the major reinsurance firms have exhibited strong appetites to fill up their portfolios in Europe and Asia Pacific once again.

In other areas of the reinsurance market, such as casualty, renewal dynamics were driven by performance and some firming was seen. While in specialty lines the market was also impacted by capacity, resulting in relatively flat dynamics.

Just how this all plays out through April renewals, when the loss affected Japan accounts renew, and June when the Floridian market comes into play, remains to be seen.

But many will be hoping for a display of greater pricing discipline at those junctures, although with capital likely to rise as the year progresses and on the ILS side funds expected to begin to release some side pocketed assets, hopes for rate increases may need to be moderated somewhat.

Read more of our reinsurance renewal coverage here.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.