Munich Re has demonstrated the power of a large diversified reinsurance and insurance group in beating its profit target for 2025, while showing its desire to retain more of the economics of its re/insurance business by slashing its retrocession arrangements and scrapping its collateralized reinsurance sidecar programme.

The global reinsurance giant beat its profit guidance for the fifth consecutive year in 2025, reporting a record net result of EUR 6.1 billion and forecasting that will rise for 2026 to EUR 6.3 billion.

The global reinsurance giant beat its profit guidance for the fifth consecutive year in 2025, reporting a record net result of EUR 6.1 billion and forecasting that will rise for 2026 to EUR 6.3 billion.

Christoph Jurecka, CEO and Chair of the Board of Management commented this morning, “2025 was a pivotal year for Munich Re. With a net result of €6.1bn, we not only set a new record, but also delivered on all the promises we had made as part of our five-year Ambition 2025 strategy programme. In times of crisis, our business model has proven to be resilient, growth-driven and profitable.

“Munich Re has consistently seized market opportunities as well as increased earnings while also stabilising them. This has allowed us to fully live up to the expectations of all stakeholders: our shareholders, customers, employees and society at large. Our new Ambition 2030 strategy programme will see us further diversify our business portfolio, expand the range of products and services we offer, and advance Munich Re as it evolves into a group that offers reinsurance, specialty insurance, and primary insurance at scale.”

The target net result was beaten in the reinsurance field of business, which remains Munich Re’s largest at this time and the profitability of reinsurance was clearly demonstrated yesterday as the company announced a further increase in share dividends and capital repatriation (as our sister publication Reinsurance News reported).

The desire to retain more of the economics of the business underwritten has been demonstrated in the retrocession arrangements Munich Re has renewed for 2026, being significantly less than a year ago.

The move also seems to demonstrate the fact that, as an increasingly diversified re/insurer, Munich Re’s peak exposures have moderated somewhat and the company perhaps feels it can manage with less tail-risk protection.

Munich Re entered 2026 with significantly less retrocessional protection in place, having only placed a retro program amounting to $600 million.

That’s down meaningfully on a retro program that amounted to $1.55 billion of protection for 2025, which utilised both traditional retro and the capital markets, through sidecars and catastrophe bonds.

It seems that, for 2026, the capital markets retro component has shrunk meaningfully for Munich Re, with the majority of its retro placed as traditional covers, albeit some are likely collateralized or fronted capital markets capacity.

For 2025, Munich Re had renewed its long-standing collateralised reinsurance sidecar structures at $650 million in size, putting this alongside $600 million of traditional retro and an outstanding $300 million of cover from the last Queen Street catastrophe bond.

For 2026, Munich Re has opted to either retire or non-renew its reinsurance sidecar program for the coming year, scrapping a meaningful source of aligned, quota share structured retrocessional protection.

Which means that, at least for now, the multi-investor Eden Re reinsurance sidecars are now more, while presumably this also means that Munich Re’s sidecar partnership with the largest insurance-linked securities end-investor PGGM under the Leo Re Ltd. structure has also been scrapped.

In addition, Munich Re’s remaining $300 million Queen Street 2023 Re dac catastrophe bond issuance that provided US hurricane retro had matured at the end of 2025 and was not renewed either.

As a result, for 2026, it appears Munich Re has only $600 million of traditional retrocession available to it, which covers it equally across its main peak peril exposures.

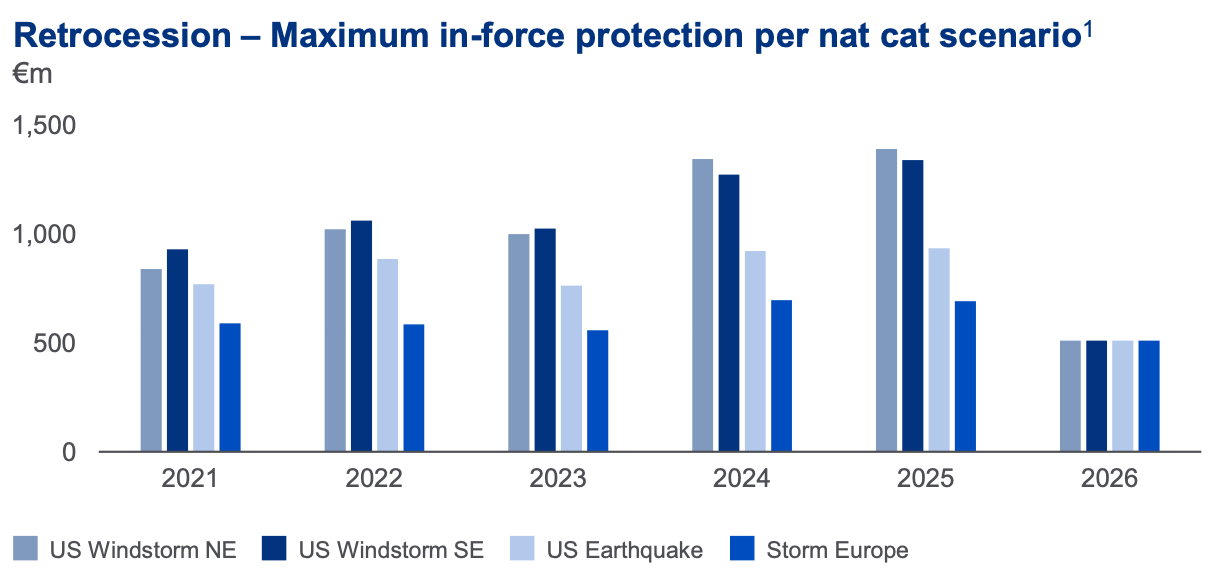

You can see how Munich Re’s catastrophe retrocession protection for peak perils has evolved below:

This is quite a bold move for a company that still has broad natural catastrophe exposure.

However, despite continuing to grow its reinsurance and insurance businesses in 2025, Munich Re’s growing diversification does mean its peak peril exposure has declined somewhat year on year, despite the retrocession program being slashed in this way.

Munich Re has reported reductions in exposure to most peak nat cat perils from 2024 to 2025, citing currency changes and portfolio management actions, offset by reductions in external retrocession. It’s not immediately clear if this remains the same for 2026, but clearly the re/insurer feels it can manage its nat cat exposure without the benefits of broader retrocessional protection in 2026.

It’s a notable shift in retro strategy, as the chart above shows that Munich Re had been steadily growing its retro protection over recent years, up until the 2026 scrapping of the sidecars and non-renewal of the catastrophe bond.

On the maintained $600 million retro program, which again is assumed to be traditional (although likely with some collateralized or ILS sourced limit), Munich Re said today that it has a, “Focus on traditional catastrophe excess of loss (CatXL) retrocession as the core format, while having the full tool case available.”

Further stating that for 2026 the, “Munich Re placement of US$ 600m benefitted from a favourable marketplace, allowing to further reshape the retrocession panel towards higher stability with less administrative efforts.”

When it comes to retro, Munich Re said it is “diligently balancing” two factors in its retro choices.

First, “price and placement volume,” and secondly, “allocations between traditional retro markets and ILS markets/investors.”

The 2026 retro program is all in traditional excess-of-loss formats and Munich Re said its well-balanced retro buying strategy reflects its strong capital base and risk-bearing capacity and a focus on expected IFRS result stabilisation in large loss scenarios.

With the increasing diversification of its business, Munich Re has been reporting that nat cat exposures are making up steadily less of its annual renewals, especially in P&C reinsurance.

Today, the company reported that at the January 2026 reinsurance renewals the volume of business written declined by 7.8%, to EUR 13.7 billion, while it said prices across its renewal book fell by 2.5%, but highlighted that the portfolio’s quality remains high and terms and conditions were importantly stable.

In fact, at January, of the P&C business that was renewable, only 15% was nat cat focused and Munich Re reports the outcome on property proportional as being a 9% volume decrease and property excess of loss as being a 13% decrease, suggesting possible further reductions in nat cat peak exposure.

Of course, being an extremely large re/insurer, Munich Re still has meaningful nat cat exposure and major catastrophe loss events from peak perils will of course drive potentially large financial impacts, but the evolution of the Munich Re business model and portfolio does mean the company appears to feel much better placed and that is perhaps also a driver of the desire to be less reliant on retrocession.

Looking ahead to the next major reinsurance renewal at April 1st, Munich Re said that it, “expects a market environment in which attractive price levels and improved terms and conditions can be largely upheld despite the current market pressure.”

The strategic shifts in retrocession buying from Munich Re show a company confident in its ability to manage its exposures, with a desire to retain more of the economics of its underwriting and that feels less need to rely on capital partners at this time.

Munich Re has never been one to follow market trends and at a time when others are ramping up retro purchases in the softer market environment, the reinsurer has taken an opposite approach for 2026.

Asked about the reduction in retro purchases during an analyst call this morning, Christoph Jurekca explained, “The basis for the way we look at retro is, of course, our strong capital base. So, we have a very strong balance-sheet and obviously our business model is a business model of a growth underwriter.

“So, therefore, if at all using retro, we do it for the purpose of managing volatility, IFRS volatility, and in light of our superior capital strength, in light also of our other options which we have to dampen volatility, we just decided that it would be better to deploy our own capital and keep the margin in house.”

You can read much more on Munich Re’s 2025 results over at Reinsurance News.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.