As much as $1.5 trillion of pension fund and private capital could be unlocked to cover climate related risks and perils according to broking group Howden, which is calling on the risk transfer industry to “change insurance for (social) good.”

Howden has looked back to previous research that found that the size of the global pension fund market’s assets under management is far larger than the insurance and reinsurance industry, suggesting that if every pension put in an average allocation to insurance-linked securities (ILS) a huge $1.5 trillion could be available to support climate risk underwriting.

It’s an updated view on an older piece of analysis, but given the timing with the COP 26 climate conference fast-approaching, it’s worth revisiting and still just as valid.

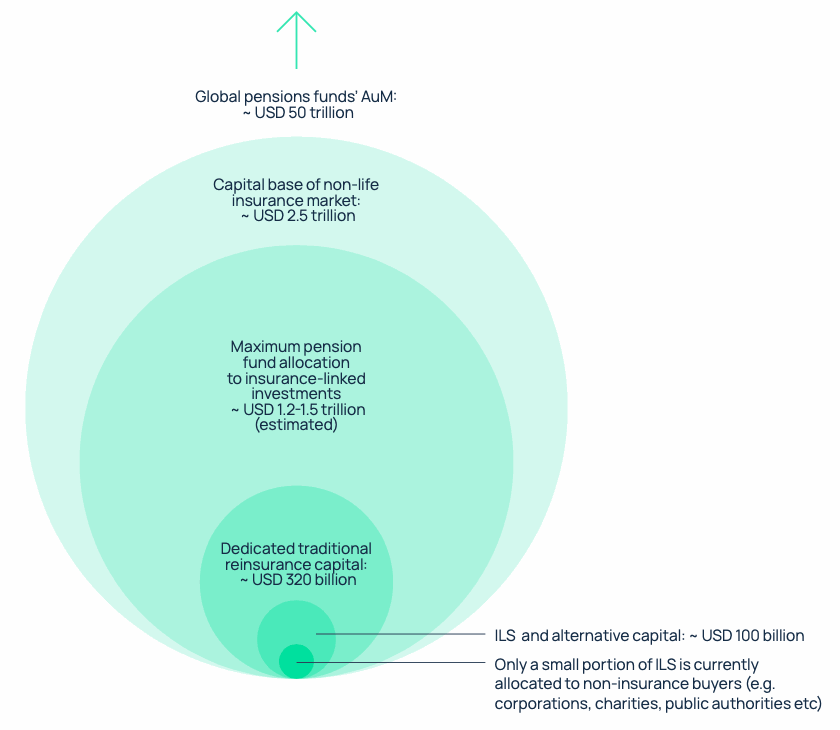

In a new report published today Howden explains, “The pool of supply provided by the ILS market for non-insurance market sponsors specifically has the potential to grow significantly. Figure 33 (above) attempts to put this into context by visualising assets under management (AuM) for global pension funds, which today are worth an estimated USD 50 trillion, together with various components that make up the total capital base of the non-life (re)insurance market.

“ILS and alternative capital is currently estimated at close to USD 100 billion, equivalent to just 4% of overall insurance and reinsurance capital, and the lion’s share of this is accessed by insurance companies.

“Howden estimates that as much as USD 1.5 trillion of total pension fund capital could be available to deploy in the (re)insurance space, highlighting the considerable capacity potential that sits within capital markets for both non-insurance and insurance market sponsors. The ILS market holds considerable appeal for investors currently, given the relatively strong rates of return (for the level of risks assumed), its uncorrelated and diversifying nature as well as the opportunity to invest in an asset class recognised (genuinely) for its environmental, social and governance (ESG) credentials.”

It’s a huge amount of capital that could potentially be unlocked for use in climate insurance, reinsurance and risk transfer.

But we’d say that the industry needs to change to achieve this, as until climate risk is structured into a truly liquid and electronically tradable capital market, it’s hard to see such numbers ever being put to work in this still relatively inefficient global insurance and reinsurance market context, including through insurance-linked securities (ILS).

But the figure should be seen as food-for-thought by decision-makers in the government’s of the world as they try to work out how to deal with burgeoning climate, weather and catastrophe risks.

The world’s capital markets and their investors are desperately searching for fixed-income alternatives to allocate to and climate and catastrophe risk could be one of those, if accessing it was made simpler, more efficient, more transparent and dare we say it, more standardised as well.

Howden’s new report highlights the trends towards rising climate costs, saying that the analysis “reinforces the link” between “the changing climate, more extreme weather events and higher insured catastrophe losses.”

But also highlights that accessibility of insurance remains a problem as well, particularly to the underserved.

David Howden, Howden Group CEO, commented, “The power of insurance both in removing barriers to the transition to a lower-carbon future, and in picking up the pieces when disaster strikes is immense. However, we cannot continue with a model that only protects those who can afford it.

“The need to deconstruct and rebuild insurance models in response to climate change is an opportunity to build back a more balanced approach, one which supports the long-term resilience of the world’s most vulnerable populations.”

In addition, the trend towards higher weather related costs in emerging economies is clear, Howden says, while so too is the widening disaster relief and humanitarian funding gap.

“Howden believes there is an opportunity for insurance to be used to create new markets and act as a force for social good by building resilience in communities without access to traditional forms of protection,” the company explained.

Which is where the capital markets can come in, as a significant and still relatively untapped source of capital with a demonstrable appetite for getting paid to assume climate, weather and catastrophe risks, as the ILS market has evidenced.

Add to that the appetite to find ESG appropriate fixed-income alternatives, which could be an enormous opportunity for disaster risk financing to be reimagined and funded at scale from institutional markets.

Charlie Langdale, Head of Climate Risk and Resilience at Howden said, “Traditional methods of disaster relief funding cannot keep pace with demand, and existing risk transfer products cannot close the protection gap. The magnitude of the issue requires something far more imaginative and innovative, something that resets how disaster relief is funded, with insurance at its core.

“The volcano catastrophe bond launched earlier this year for the Danish Red Cross has proven that insurance-based products can bring together charitable donations and private capital in a way that provides more funds, more quickly to those who need it. Scaling this model up unlocks significant potential to address the imbalance in accessibility, whilst creating an attractive market for investors.”

Howden concluded, “I am convinced that what we have achieved with the Red Cross will prove to be a game changer. By focusing our collective expertise, data and ingenuity on creating new markets, we can unlock the huge sums of private capital looking for environmentally and socially conscious investments. This isn’t about tweaking existing models, it is about reinventing risk transfer and creating completely new markets. This is about changing insurance for good.”

We would add that, to change insurance for good and truly connect these enormous capital pools with climate, weather and catastrophe risks, market structure and the mode of transferring risk from primary clients, via reinsurance and right through to sources of retrocessional capital, needs updating and the industry needs to redouble its focus on cost and removing fat (expense) from the transaction.

But we certainly agree that now is the time to raise this opportunity and highlight the availability of capital to absorb some of the world’s climate risks, as long as they are well-structured, delivered efficiently and have lower costs attached to the transaction process itself.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.