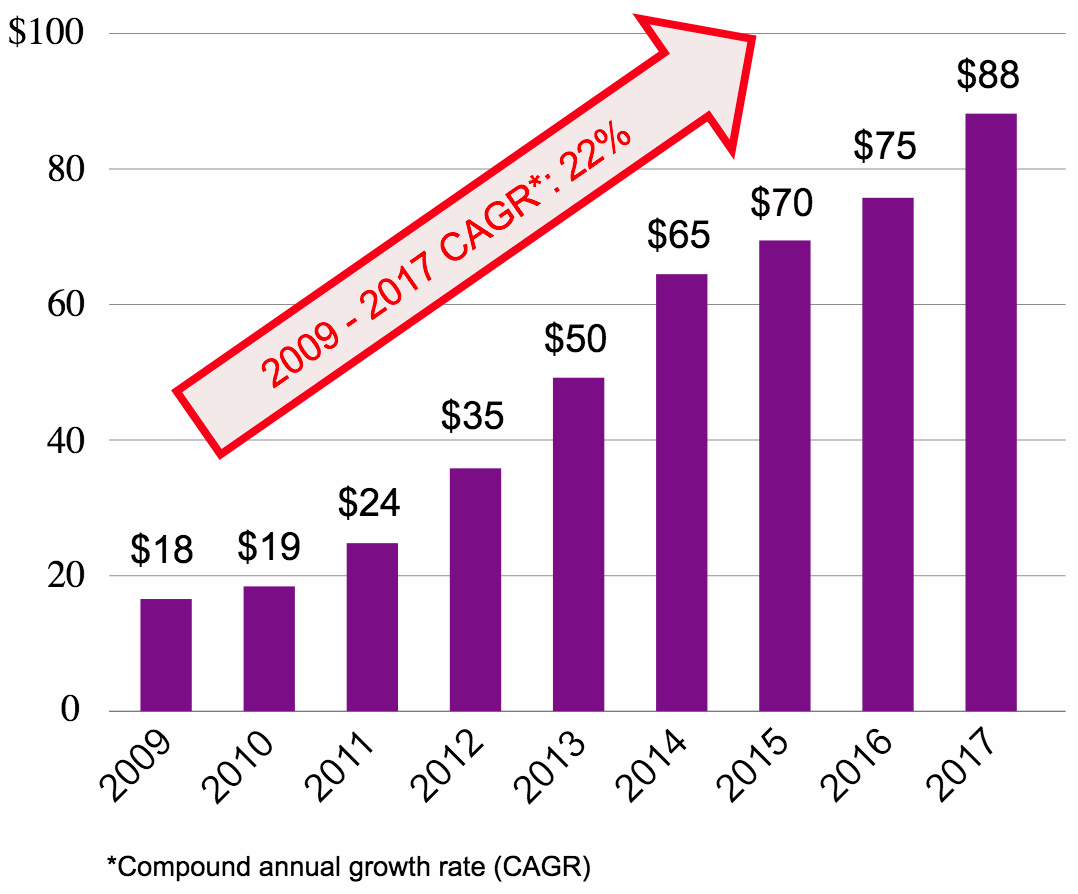

According to the latest market data from capital markets and insurance-linked securities (ILS) brokerage unit Willis Towers Watson Securities (WTWS), the amount of non-life ILS capital in reinsurance markets grew by a stunning 17% over the course of 2017, to reach $88 billion.

This is despite the major catastrophe losses that the market experienced in the third and fourth-quarters of last year, which WTWS notes is a demonstration that, “The ILS market was able to withstand the 2017 natural catastrophe losses as funds diligently reached out to their investors and risk partners ensuring an orderly and supportive environment.”

The estimate for $88 billion of non-life ILS capital at year-end 2017 is not far off the $87 billion we have recorded in the Artemis Insurance Linked Securities (ILS) Investment Managers & Funds Directory, but add in the direct investors and other reinsurer managers, sidecars etc not in our Directory and we estimate the total to be well on the way to $100 billion. When including life ILS capital it could even be higher.

WTWS said that it expects that 2018 will be, “Another year of growth for insurance linked securities (ILS) as the market recovers from recent natural disasters, replaces lost capital and investors show mounting interest in ILS products.”

The broker unit saw ILS capital at $75 billion at the end of 2016, but over the course of 2017 and thanks largely to the post-loss fund-raising efforts of ILS fund managers, the market grew by 17% to reach $88 billion.

Year-end ILS capital outstanding ($bn) - From Willis Towers Watson Securities

As you can see from the chart above, taken from Willis Towers Watson Securities latest quarterly ILS market report, the ILS market has grown at a compound rate of 22% between 2009 and the end of 2017, an impressive rate of growth.

WTWS also said the impressive growth of ILS capital seen in 2017, “Rather than running away from the losses, ILS capital is running toward both the short-term potential for modestly better risk spreads and the longer term 20 opportunity to partner with reinsurers, insurers and insureds to fuel asset under management (AUM) growth and ultimately make insurance more available and affordable.”

That’s an important distinction, as the growth of capital is not purely on a short-term basis, seeking to profit from higher rates. In fact relatively little of the ILS capital raised towards the end of 2017 has been for specific post-event strategies, while more has been allocated to the normal long-term ILS fund strategies, which will benefit from a return boost, but are not typically seen as speculative allocations.

Bill Dubinsky, Managing Director and head of ILS, Willis Towers Watson Securities, commented on the outlook for the market, saying, “We see no end in sight to ILS growth. The ILS community is signalling that it is ready and open for business.

“2018 is shaping up as a brutal battle for market share between, on the one hand, incumbent reinsurers and ILS investors trying to both maintain their positions and exact some rate increases and, on the other hand, other ILS investors and reinsurers trying to stake a claim to participate in additional risk.”

The report notes the trend for larger, more established ILS investors to have taken some share off reinsurers at 1/1, but says that in some cases these often customised arrangements, see ILS investors taking a leaf out of the reinsurers books and playing the relationship card.

WTWS continues to push for a more syndicated approach, less bilateral collateralized reinsurance, noting that “liquid ILS capacity is plentiful with modest spread changes relative to stickier placements.”

WTWS warns that, “The relationship hug sometimes turns into a sucker punch,” as cedents can become too reliant on too few larger capacity sources.

The broker is clearly hoping for more catastrophe bond and syndicated ILS transactions in 2018, something the market would support as well.

For the larger ILS managers that have deepened their relationships with select, major cedents, the strategy does see them accessing a much broader world of risk and it does seem this will make hedging ILS portfolios even more important through the rest of this year.

![]() View all of our Artemis Live video interviews and subscribe to our podcast.

View all of our Artemis Live video interviews and subscribe to our podcast.

All of our Artemis Live insurance-linked securities (ILS), catastrophe bonds and reinsurance video content and video interviews can be accessed online.

Our Artemis Live podcast can be subscribed to using the typical podcast services providers, including Apple, Google, Spotify and more.